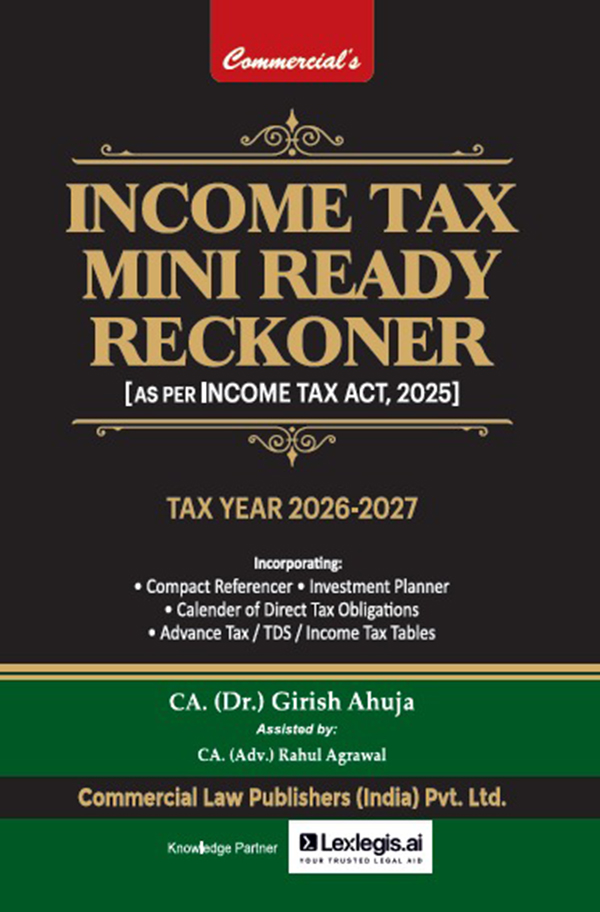

Income Tax Mini Ready Reckoner

Original price was: ₹1,195.00.₹896.00Current price is: ₹896.00.

| Book Details | |

| Title | Income Tax Mini Ready Reckoner for Tax Year 2026-27 as per Income Tax Act, 2025 |

| ISBN | 978-93-7833-802-1 |

| Edition | 29th Edition 2026 |

| Pages | 992 |

| Authors | Dr. Girish Ahuja CA (Adv.) Rahul Aggarwal |

| Publisher | Commercial Law Publishers |

(Flat 25% Discount for a limited period + Free Shipping)

- Description

- Additional information

- Reviews (0)

Description

Income Tax Mini Ready Reckoner – 29th Edition (2026) for Tax Year 2026-27 as per Income Tax Act, 2025 is a concise yet comprehensive guide designed for quick reference and efficient income tax computation and planning. Authored by Dr. Girish Ahuja and CA (Adv.) Rahul Aggarwal, and published by Commercial Law Publishers, this book is widely trusted by tax professionals and students.

With 992 pages of structured and easy-to-navigate content, the book provides ready reference tables, tax rates, deductions, exemptions, and computation guidelines, enabling quick decision-making and accurate tax compliance.

This publication is highly useful for chartered accountants, tax practitioners, consultants, finance professionals, academicians, and students who require a handy and reliable reference for income tax planning and day-to-day practice.

📘 Key Features:

- Compact yet comprehensive income tax ready reckoner

- Includes tax rates, deductions, exemptions & computation tables

- Designed for quick reference and practical use

- Authored by leading experts in taxation

🎉 Limited-Period Offer: Flat 25% Discount with Free Shipping

About the Authors

Dr. GIRISH AHUJA did his graduation and postgraduation from Shri Ram College of Commerce, Delhi and was a position holder. He was awarded a Ph.D. degree by Faculty of Management Studies (FMS), Delhi University. He is a Fellow of the Institute of Chartered Accountant of India (ICAI) and was a rank holder of both Intermediate and Final examinations of the Institute. He had been nominated by the Government of India as a member of the Task Force for redrafting the Income-tax Act and New Income-tax Law. He is also on the Board of Directors of many reputed companies and has a vast and rich experience in the field of finance and taxation. He has been nominated by the Government as member of Board of Directors of UNITECH LTD with the approval of the Supreme Court and was also been nominated by the Govt. of India as Independent Director of the Central Board of State Bank of India. Dr. Ahuja is a author of various books on Direct Taxation and he has addressed more than 5000 seminars organized by the ICAI, ICSI, ICWAI, Chambers of Commerce.

Content

| Chapter | Content | Page |

| DIVISION 1 | Compact Referencer | |

| CR-1 | Amendments brought in the Income-Tax Act, 2026 by the Finance Act, 2026 | 1 |

| CR-2 | Rates of Taxation | 47 |

| CR-3 | Direct Tax Rates for Last Ten Assessment Years | 67 |

| CR-4 | Cost Inflation Index & Exemptions Available in Computation of Capital Gain | 82 |

| CR-5 | TDS & TCS at a glance86 | |

| CR-6 | Time Limit, Form & Fees for Filing an Appeal | 101 |

| CR-7 | Prescribed Audit Reports under the Income-tax Rules/Act | 103 |

| CR-8 | Prescribed Reports/Certificates from an Accountant | 105 |

| CR-9 | Gold & Silver Rates since 1-4-2001 | 107 |

| CR-10 | Investment Planner | 109 |

| CR-11 | Repeal and Savings | 129 |

| DIVISION 2 | Income Tax | |

| 1 | Introduction | 137 |

| 2 | Scope of Total Income & Residential Status [Sections 5 to 9B] | 148 |

| 3 | Incomes which do not Form Part of Total Income | 172 |

| 4 | HComputation of Total Income [Sections 13 & 14] & Income under the Head “Salaries” [Sections 15 to 19] |

201 |

| 5 | Income under the Head “Income from House Property” [Sections 22 to 25] | 276 |

| 6 | Income under the Head “Profits and Gains of Business or Profession” [Sections 26 to 66] | 289 |

| 7 | Income under the Head “Capital Gains” [Sections 67 to 91] | 371 |

| 8 | Income under the Head “Income from Other Sources” [Sections 92 to 95] |

489 |

| 9 | Income of Other Persons included in Assessee’s Total Income (Clubbing of Income) [Sections 96 to 100] |

506 |

| 10 | Unexplained Cash Credits, Investments, Money, etc. [Sections 102 to 107] | 515 |

| 11 | Set off or Carry Forward and Set off of Losses [Sections 108 to 121] | 520 |

| 12 | Deductions to be made in Computing Total Income [Sections 122to 154) | 539 |

| 13 | Agricultural Income & its Tax Treatment [Sections 2(5) and 11 | 583 |

| 14 | Computation of Tax Liability of Various Categories of Persons | 589 |

| 15 | Return of Income and Procedure of Assessment [Sections 262 to 291] | 628 |

| 16 | Permanent Account Number and Aadhaar Number [Section 390 to 402] | 702 |

| 17 | Advance Payment of Tax [Sections 207-211, 403 to 410] | 770 |

| 18 | Interest and Fee Payable [Sections 398(3), 411(3), 411(6), 423, 424, 425, 426, 427, 428, 429, 430 & 437 (Erstwhile Sections 201(1A), 206C(7), 220(2), 234A, 234B, 234C, 234D, 234E, 234F, 234G,234H & 244A] |

778 |

| 19 | Refunds [Sections 431 to 438 (Erstwhile Section 237 to 241 & 245)] | 805 |

| 21 | Penalties and Prosecutions [Sections 298, 412 & 439 to 491] | 810 |

| 22 | Appeals and Revisions [Sections 356 to 378] | 852 |

| 23 | Miscellaneous Provisions | 877 |

Additional information

| Publisher | Commercial |

|---|

Reviews

There are no reviews yet.