Financial Fitness- Ensuring Financial Stability Through Timely Payments In MSE

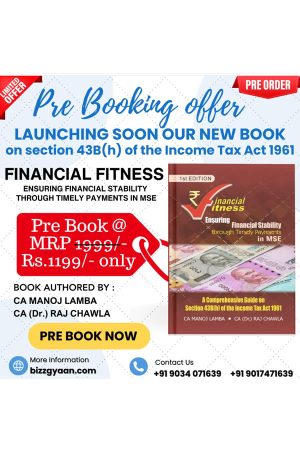

Original price was: ₹1,999.00.₹1,199.00Current price is: ₹1,199.00.

| Book Details | |

| Title | Financial Fitness- Ensuring Financial Stability Through Timely Payments In MSE |

| ISBN | 978-93-340-3431-8 |

| Edition | Edition 1st |

| Pages | 354 |

| Authors | CA Manoj Lamba and CA (Dr) Raj chawla |

| Publisher | CA Manoj Lamba |

(Flat 40% Discount for a limited period + Free Shipping)

- Description

- Additional information

- Reviews (0)

Description

Discover “Financial Fitness,” the guide to ensuring financial stability through timely payments in MSEs. This book covers tax laws, MSE payments, compliance measures, and more, with detailed chapters, contents, and page references. Grab your copy now for insights into optimizing financial health! authored by CA Manoj Lamba and CA (Dr) Raj Chawla.

Financial Fitness: Ensuring Financial Stability through Timely Payments in MSE

“Financial Fitness” is a comprehensive guidebook authored by CA Manoj Lamba and CA(Dr) Raj Chawla, aimed at providing a detailed understanding of Section 43B(h) of the Income Tax Act, 1961. This book serves as a valuable resource for individuals and businesses, particularly Micro and Small Enterprises (MSEs), seeking to enhance their financial stability through timely payments.

The primary objective of “Financial Fitness” is to elucidate the significance and implications of the amendment to Section 43B(h) of the Income Tax Act, 1961. This amendment was introduced with the aim of ensuring timely payments to MSEs, thereby safeguarding their financial interests and promoting their overall stability. By providing a comprehensive guide on this amendment, the authors aim to empower readers with the knowledge and tools necessary to navigate the intricacies of tax compliance related to payments to MSEs.

Key Features:

Practical Examples: The book is enriched with numerous practical examples illustrating the application of Section 43B(h) in various scenarios. These examples help readers understand the practical implications of the amendment and its relevance to real-world situations.

Multiple-Choice Questions (MCQs): To facilitate interactive learning, “Financial Fitness” includes MCQs at the end of each chapter. These MCQs not only reinforce key concepts but also aid in self-assessment and preparation for examinations or assessments related to tax compliance.

Numericals: Complex numerical problems related to Section 43B(h) are presented in a simplified manner, allowing readers to practice calculations and gain proficiency in applying the provisions of the Income Tax Act.

Case Studies: The inclusion of detailed case studies offers readers insights into how businesses can effectively manage their tax obligations while ensuring compliance with the provisions of Section 43B(h). These case studies provide practical insights and solutions to common challenges faced by MSEs.

Flowcharts: Complex processes and procedures are simplified through the use of flowcharts, providing readers with a visual aid to understand the sequential steps involved in complying with the provisions of Section 43B(h).

Colorful Design and Meaningful Pictures: The book’s visually appealing design, complemented by meaningful pictures, enhances readability and engagement. Colorful illustrations and graphics are strategically used to break down complex concepts and make the content more accessible to readers.

Conclusion: “Financial Fitness” stands as a testament to the diligent efforts of CA Manoj Lamba and CA(Dr) Raj Chawla in demystifying the provisions of Section 43B(h) of the Income Tax Act, 1961. Through its comprehensive coverage, practical examples, MCQs, numericals, case studies, and visually appealing design, the book serves as an indispensable guide for individuals and businesses striving to achieve financial stability through timely payments in MSEs. It not only educates but also empowers readers to navigate the intricacies of tax compliance with confidence and proficiency.

INDEX

| Chapter | Contents | Pages |

|---|---|---|

| 1 | INTRODUCTION TO SECTION 43B (h) OF INCOME TAX ACT 1961 | 1 – 14 |

| 2 | WHETHER TRADERS ARE LIABLE FOR DISALLOWANCE U/S 43B (h)? | 15-35 |

| 3 | Whether UDYAM REGISTRATION is Mandatory or Not? | 36-46 |

| 4 | APPLICABILITY OF SECTION 43B(h) ON TAXPAYERS FOLLOWING PRESUMPTIVE TAXATION SCHEME U/S 44AD/44ADA/44AE? | 47-59 |

| 5 | Will the GST component be disallowed if the sum payable to MSE attracts Section 43B(h) disallowance? | 60-66 |

| 6 | WHETHER terms mentioned on the invoice or purchase order SHOULD be treated as an agreement? | 67-83 |

| 7 | WHICH ENTERPRISE ARE COVERED UNDER MICRO AND SMALL ENTERPRISE? | 84-96 |

| 8 | Calculation of Turnover and Investment for Classification of MSME | 97-109 |

| 9 | WHAT IS TIME LIMIT PRESCRIBED FOR MAKING PAYMENT UNDER SECTION 15 OF MSMED ACT 2006? | 110-118 |

| 10 | What is meant by the terms “the Appointed Day”, “the day of acceptance”, and “the day of deemed acceptance”? | 119-127 |

| 11 | Whether Section 43B(h) disallowance will also apply with respect to the amounts due towards the purchase of Capital Goods? | 128-134 |

| 12 | Can disallowance under Section 43B(h) be made while computing book profit for MAT purposes? | 135-142 |

| 13 | Will Section 43B(h) apply to fees payable to a CA firm? | 143-151 |

| 14 | If the assessee follows a cash system of accounting, it will not hit by section 43B(h) of Income Tax Act-1961? | 152-157 |

| 15 | What if any charitable trust is making payment to an MSME? Will Section 43B(h) apply? | 158-164 |

| 16 | Are old outstanding dues to Micro and Small Enterprises (MSE) as of April 1, 2023, or any earlier period subject to disallowance under section 43B(h)? | 165-170 |

| 17 | Issue for consideration Section 43B of the Income Tax Act provides that certain deductions shall be allowed only in that previous year in which the specified sum is actually paid, irrespective of the previous year in which the liability to pay such sum was incurred according to the method of accounting regularly employed by the assessee. | 171-187 |

| 18 | How the various payment made to micro and small enterprises are appropriated while calculating the disallowance under section 43B(h) of Income Tax Act-1961? | 188-197 |

| 19 | Effective Date of Payment in case Payment by Cheque | 198-205 |

| 20 | STATUTORY VS CONTRACTUAL DUES | 206-212 |

| 21 | Whether disallowance under section 43B(h) in respect of outstanding dues to micro and small Enterprise would amount to deferred Tax Asset and required consideration in financial statements? | 213-220 |

| 22 | Whether provisions appearing in balance sheet as on 31-03-2024 in respect of certain deduction/ expenses in respect of audit fee, legal fee, accounting charges etc are liable for disallowance under section 43B(h) of income Tax Act-1961? | 221-227 |

| 23 | How can an assessee identify that his supplier is a micro or small enterprise? | 228-237 |

| 24 | Whether interest under section 16 of MSMED Act 2006 is mandatory or optional? | 238-250 |

| 25 | Amount of Interest inadmissible under section 23 of the Micro, Small and Medium Enterprises Development Act, 2006 [Clause 22 of Form No.3CD for Tax Audit u/s 44AB of Income Tax Act-1961] | 251-265 |

| 26 | Changes in Indian Income Tax Return to Give Effect to Amendment of Section 43B(h) of Income Tax Act, 1961 | 266-275 |

| 27 | Comprehensive Analysis of Amendments to Form 3CD Regarding Delayed Payments to MSEs | 276-288 |

| 28 | Reporting Requirement as per Revised Schedule III of Companies Act, 2013, Regarding New Aging Schedule of Creditors and Its Impact on Calculation of Disallowance under Section 43B(h) of Income Tax Act, 1961, and Payment of Interest under Section 16 of MSMED Act, 2006 | 289-293 |

| 29 | Whether section 43B(h) disallowance also applicable on purchases directly debited to stock in trade or purchase lying in stock in trade at Year end ? | 284-296 |

| 30 | Whether Disallowance under Section 43B (h) reversible in the year of actual payment ? | 296-304 |

| 31 | What if the due date for payment falls on a public holiday or national holiday? Would a payment made on the next working day be considered effective for the purposes of Section 43B(h) of the Income Tax Act, as well as for Sections 15, 16, and 23 of the Micro, Small and Medium Enterprises Development (MSMED) Act? | 305-306 |

| 32 | OPPORTUNITIES FOR PROFESSIONALS AND BUSINESSES | 307-309 |

| 33 | Auditor’s role in ensuring compliance with Section 43B(h) of the Income Tax Act-1961 | 310-312 |

| 34 | Whether issue of equity shares or debentures to Micro and Small Enterprise (MSE) suppliers will amount to Actual Payment ? | 313-316 |

| 35 | Case Study | 317-330 |

Additional information

| Publisher | Manoj Lamba |

|---|

Reviews

There are no reviews yet.