-25%

-Act,-2010-1")

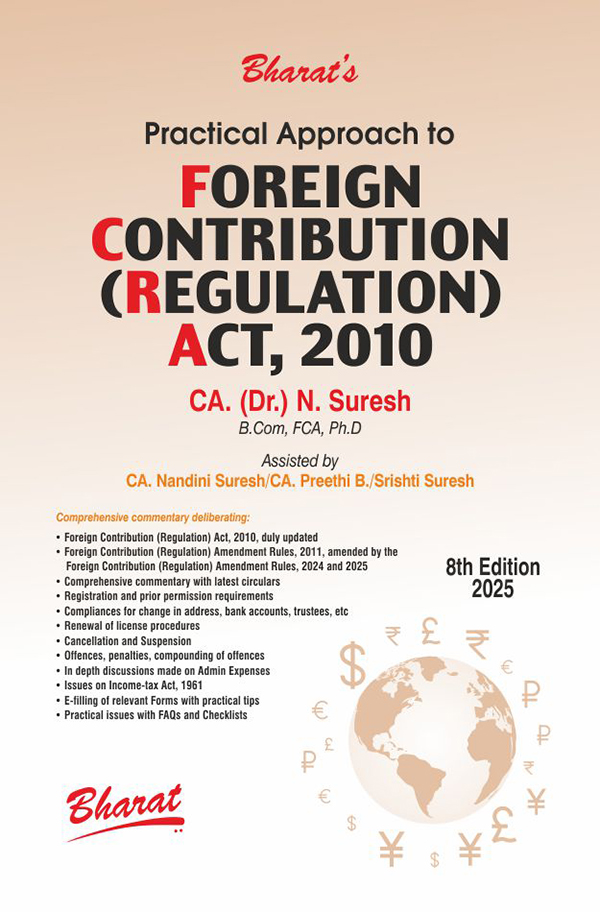

Practical Approach to Foreign Contribution (Regulation) Act, 2010

Original price was: ₹1,895.00.₹1,421.00Current price is: ₹1,421.00.

| Book Details | |

| Title | Practical Approach to Foreign Contribution (Regulation) Act, 2010 |

| ISBN | 978-93-4808-039-4 |

| Edition | 8th edn., 2025 |

| Pages | 832 |

| Authors | CA. (Dr.) N. Suresh |

| Publisher | Bharat Publishers |

(Flat 25% Discount for a limited period + Free Shipping)

- Description

- Additional information

- Reviews (0)

Description

Order the “Practical Approach to Foreign Contribution (Regulation) Act, 2010,” 8th edition (2025) by CA (Dr.) N. Suresh. This comprehensive 832-page guide, published by Bharat Publishers, provides practical insights into the Foreign Contribution (Regulation) Act, 2010. Available with a flat 25% discount for a limited period and free shipping. Get your copy now using ISBN 978-93-4808-039-4 to understand FCRA regulations and compliance better.

DETAILED CONTENTS

| Chapter | Content | Page |

| Bharat? | 5 | |

| Preface to the Eighth Edition | 7 | |

| About the Author | 9 | |

| About the Experts who have contributed to the Book | 11 | |

| Detailed Contents | 17 | |

| Table of Cases | 49 | |

| 1 | Introduction to FCRA | 1 |

| 2 | Applicability of FCRA | 5 |

| 3 | Amendments made by Foreign Contribution (Regulation) Amendment Rules, 2015 | 10 |

| 4 | Foreign Contribution | 28 |

| 5 | Foreign Contribution — Exceptions | 38 |

| 6 | Foreign Hospitality | 41 |

| 7 | Foreign Source | 65 |

| 8 | Foreign Company | 72 |

| 9 | Prohibition to Accept Foreign Contribution | 76 |

| 10 | Foreign Contribution versus Commercial Organisations | 80 |

| 11 | Organisation of Political Nature | 82 |

| 12 | Associations or Company Engaged in Production or Broadcast of Audio News or Audio Visual News | 89 |

| 13 | Permissible Activities | 100 |

| 14 | Gift from Relatives and Foreign Sources | 103 |

| 15 | Registration — Procedure and Compliances | 107 |

| 16 | Prior Permission — Procedure and Compliances | 148 |

| 17 | Circumstances for Rejection of Application for Registration and Prior Permission | 174 |

| 18 | Grant of Certification of Registration and Prior Permission | 178 |

| 19 | Renewal of Registration | 185 |

| 20 | Suspension of Registration | 210 |

| 21 | Cancellation of Registration | 218 |

| 22 | Designated Bank Accounts | 230 |

| 23 | Change in Bank Account — Procedure | 248 |

| 24 | Responsibility of Banks under FCRA, 2010 | 250 |

| 25 | Administrative/Establishment Expenses and Speculative Investments | 272 |

| 26 | Books of Accounts and Method of Accounting | 284 |

| 27 | Audit of Accounts and Filing of Returns | 291 |

| 28 | Legal Due Diligence | 301 |

| 29 | Custody and Management of Foreign Contribution and Assets | 308 |

| 30 | FCRA Assets — Investments and Fixed Assets | 312 |

| 31 | Procedure for Change in Name, Aims, Objectives, Address | 314 |

| 32 | Funds Transfer to Unregistered Organisations | 320 |

| 33 | International Activities, Transfers | 324 |

| 34 | NRI or Foreign National can be a Board Member | 335 |

| 35 | Composition of Change in Board Members | 339 |

| 36 | Funds – Loans – Domestic and Other Sources | 345 |

| 37 | Funds — Internally Generated, Borrowings, Voluntary Contributions | 347 |

| 38 | Foreign Contribution Received in Kind | 352 |

| 39 | Inspection, Search and Seizure | 356 |

| 40 | Appeals under FCRA, 2010 | 364 |

| 41 | Revision of Order by Central Government | 367 |

| 42 | Offences and Penalties | 371 |

| 43 | Compounding of Offences | 382 |

| 44 | Power to Make Rules | 390 |

| 45 | Power to Remove Difficulties | 393 |

| 46 | Central Government’s Power to Exempt and Other Powers | 394 |

| 47 | Application of Other Laws not Barred | 395 |

| 48 | Repeal and Saving | 356 |

| 49 | Whether FCRA will Apply to Central or State Government Organisations | 398 |

| 50 | Projects Grants, Grant-in-Aid — Applicability of FCRA | 400 |

| 51 | Liaison and Branch Office of Foreign Trust or Institution — Activities in India | 404 |

| 52 | Corporate Social Responsibility | 442 |

| 53 | Frequently Asked Questions (with Additional Questions), Circulars, Charters, etc. | 480 |

| 54 | Foreign Contribution (Regulation) Act, 2010 as amended upto date | 515 |

| 55 | Foreign Contribution (Regulation) Rules, 2011 as amended upto date |

548 |

| 56 | Prevention of Money Laundering Act, 2002 as applicable to NPOs | 584 |

| 57 | Filling of Annual Returns of Assets and Liabilities under Lokpal and Lokayukta Act, 2013 by Individual of an Association | 600 |

| 58 | Practical Case Studies | 606 |

| 59 | Practical Illustration of Form FC-1 | 612 |

| 60 | Practical Illustration of Form FC-2 | 617 |

| 61 | Practical Illustration of Form FC-3A | 621 |

| 62 | Practical Illustration of Form FC-3B | 627 |

| 63 | Practical Illustration of Form FC-3C | 636 |

| 64 | Practical Illustration of Form FC-4 | 641 |

| 65 | Practical Illustration of Form FC-6A | 649 |

| 66 | Practical Illustration of Form FC-6B | 651 |

| 67 | Practical Illustration of Form FC-6C | 653 |

| 68 | Practical Illustration of Form FC-6D | 656 |

| 69 | Practical Illustration of Form FC-6E | 658 |

| 70 | Practical Illustration of Form FC-7 | 660 |

| 71 | Charity | 662 |

| 72 | Charitable Purpose | 664 |

| 73 | Relief of Poor | 668 |

| 74 | Education and Medical Relief | 671 |

| 75 | Advancement of any Other General Public Utility | 680 |

| 76 | Basics of Formation of Trust, Society, Section 8 Company | 672 |

| 77 | Formation of Trust | 695 |

| 78 | Formation of a Society (under the Societies Registration Act, 1860) | 704 |

| 79 | Formation of Section 8 Company | 709 |

| 80 | Registration of Trust under section 12A | 720 |

| 81 | Procedure for Registration of Trust or Institution under section 12AA/12AB | 729 |

| 82 | Income of Charitable or Religious Trusts or Institutions | 748 |

| 83 | Application of Income | 753 |

| 84 | Prescribed Mode of Investment | 760 |

| 85 | Overview of Forfeiture of Exemption | 767 |

| 86 | Taxation of Charitable or Religious Trusts or Institutions | 771 |

Additional information

| Publisher | Bharat |

|---|

Reviews

There are no reviews yet.