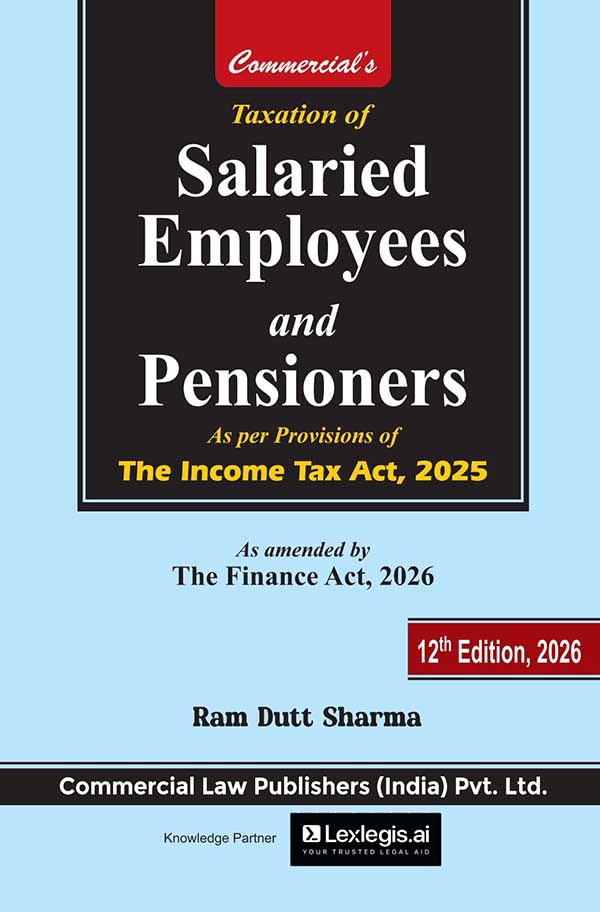

Taxation of Salaried Employees and Pensioners

Original price was: ₹695.00.₹521.00Current price is: ₹521.00.

| Book Details | |

| Title | Taxation of Salaried Employees and Pensioners |

| ISBN | 9789378332258 |

| Edition | 12th Edition 2026 |

| Pages | 288 |

| Authors | Ram Dutt Sharma |

| Publisher | Commercial Law Publishers |

(Flat 25% Discount for a limited period + Free Shipping)

- Description

- Additional information

- Reviews (0)

Description

Taxation of Salaried Employees and Pensioners – 12th Edition (2026) is a practical and easy-to-understand guide focused on income tax provisions applicable to salary earners and pension recipients. Authored by Ram Dutt Sharma and published by Commercial Law Publishers, this book simplifies tax compliance for individuals.

With 288 pages of clear and structured content, the book covers key topics such as salary income computation, allowances, perquisites, deductions, exemptions, tax planning strategies, pension taxation, and filing of income tax returns. It is designed to help readers understand their tax liabilities and optimize their tax planning.

This publication is highly useful for salaried individuals, pensioners, tax consultants, chartered accountants, HR professionals, and students seeking clarity on personal taxation.

📘 Key Features:

- Focused coverage of salary and pension taxation

- Includes deductions, exemptions & tax planning tips

- Simple and practical explanations for easy understanding

- Suitable for individuals and professionals alike

🎉 Limited-Period Offer: Flat 25% Discount with Free Shipping

| Chapter | Content | Page |

| 1 | Introduction | 1 |

| 2 | Essential Characteristics of Salary | 6 |

| 3 | Different Forms of Salary | 10 |

| 4 | Salary not treated as Income under the head ‘Salary | 14 |

| 5 | Exempted Salary | 20 |

| 6 | “income” includes | 23 |

| 7 | Scope of Total Income | 25 |

| 8 | Income deemed to accrue or arise in India | 28 |

| 9 | Basis for charging income under the head ‘Salaries’ | 31 |

| 10 | Income from Salary | 41 |

| 11 | Perquisite | 45 |

| 12 | Valuation of perquisites | 56 |

| 13 | Profits in lieu of salary | 71 |

| 14 | Deductions from Salaries | 80 |

| 15 | Treatment of Retirement Benefits | 82 |

| 16 | Allowances which are Fully Exempt | 103 |

| 17 | Allowances which are Partially Taxable | 109 |

| 18 | Allowances – Exemption depends upon actual expenditure by the employee |

114 |

| 19 | Allowances to meet personal expenses which are exempt to the extent of amount received or the limit specified, whichever is less. |

122 |

| 20 | Allowances which are Fully Taxable | 136 |

| 21 | Taxability of various Funds | 138 |

| 22 | Taxability of Salary of Foreign Citizen | 145 |

| 23 | Deductions to be made in computing Total Income from Salary | 150 |

| 24 | Rebate of Income-tax in case of certain Individualsy | 204 |

| 25 | Relief when salary, etc., is paid in Arrears or in Advance | 207 |

| 26 | New Tax Regime – Lower Tax Rate Option | 218 |

| 27 | Income Tax Rates [Old Tax Regime]. | 227 |

| 28 | Income Tax Deduction at Source from Salary | 238 |

| 29 | Taxation of Pensioners | 252 |

| 30 | Computation of Income from Salary | 272 |

Additional information

| Publisher | Commercial |

|---|

Reviews

There are no reviews yet.